BARBADOS PUBLIC WORKERS’ CO-OPERATIVE CREDIT UNION LIMITED

NON-CONSOLIDATED ANNUAL REPORT 2015

52

BARBADOS PUBLIC WORKERS' CO-OPERATIVE CREDIT UNION LIMITED

Notes to the Non-consolidated Financial Statements

For the year ended March 31, 2015

(Expressed in Barbados dollars)

41

23. Commitments and Contingencies...(continued)

(iv) Lease commitments

The Credit Union leases branch facilities under operating leases. Payments made under these

leases are recognised in the statement of income on a straight-line basis over the term of the lease.

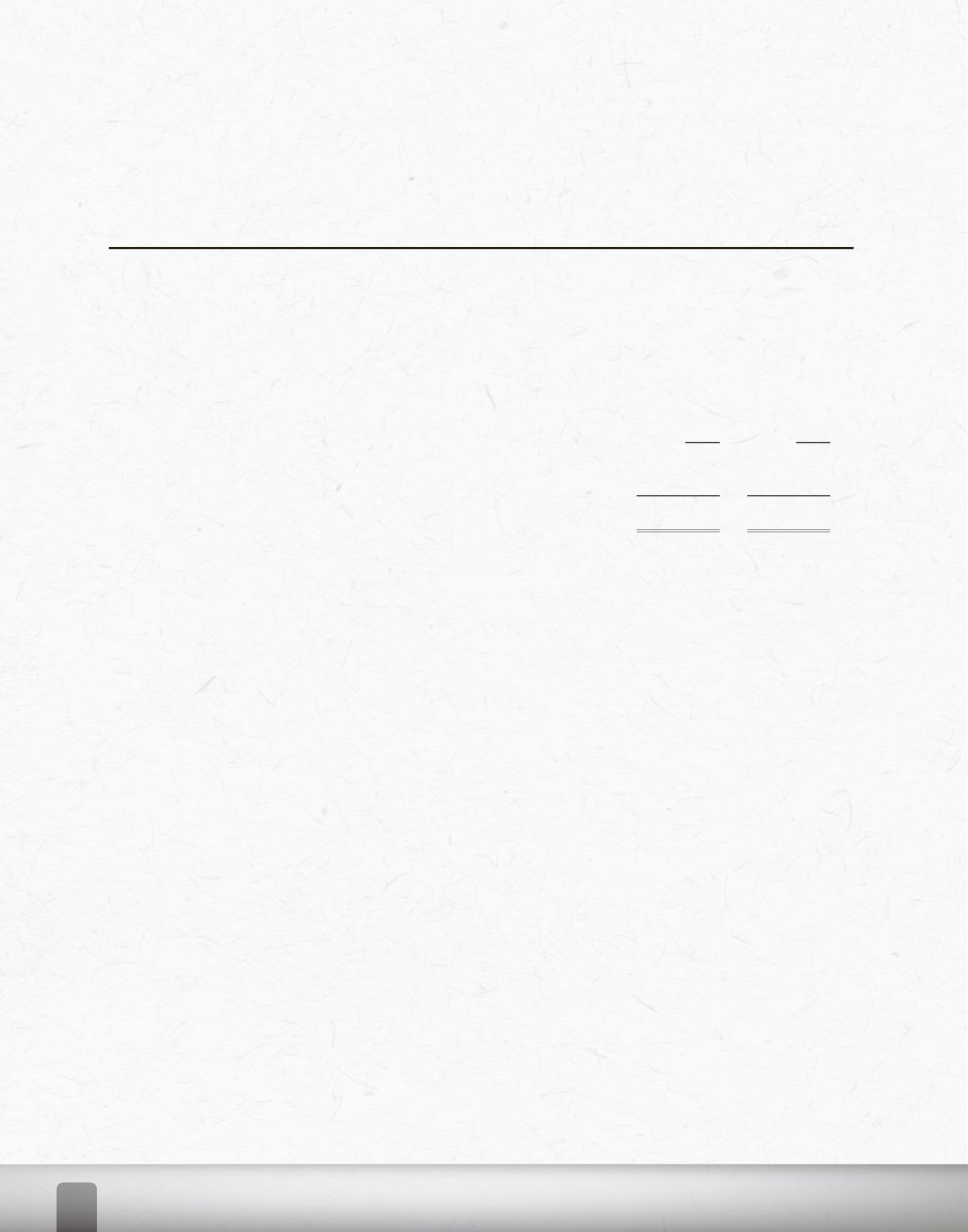

The future minimum rental payments related to these commitments are as follows:

2015

2014

Less than one year

$

627,265

296,196

Between one and five years

2,903,100

1,184,784

$ 3,530,365

1,480,980

During the year, $753,149 (2014 - $285,915) was recorded as an expense in the statement of

income in respect of operating leases.

24. Financial Risk Management

Introduction

Risk is inherent in the Credit Unionʼs activities but is managed through a process of on-going

identification, measurement and monitoring, subject to risk limits and other controls. This process of risk

management is critical to the Credit Unionʼs continuing profitability and each individual is accountable

for the risk exposures relating to his or her responsibilities. The Credit Union is exposed to credit risk,

liquidity risk, market risk and operational risk.

The Credit Unionʼs aim therefore is to achieve an appropriate balance between risk and return and

minimise potential adverse effects on its financial performance.

The independent risk control process does not include business risks such as changes in the

environment, technology and industry. The Credit Union's policy is to monitor those business risks

through its strategic planning process.

Risk management structure

The Board of Directors is responsible for the overall risk management approach and for approving the

risk management strategies and principles.

The Supervisory Committee has the responsibility to monitor the overall risk process within the Credit

Union.

The Credit Unionʼs policy is that risk management processes are audited annually by the Internal Audit

function, which examines both the adequacy of the processes and the Credit Unionʼs compliance with

the processes. Internal Audit discusses the results of all assessments with management, and reports its

findings and recommendations to the Supervisory Committee.